Banks' bad loans unexpectedly ease from record

MANILA, Philippines — Bad loans by banks surprisingly declined for the first time in a year in December, helping keep their levels in check against expectations of a drastic increase due to pandemic-scarred borrowers defaulting on payments.

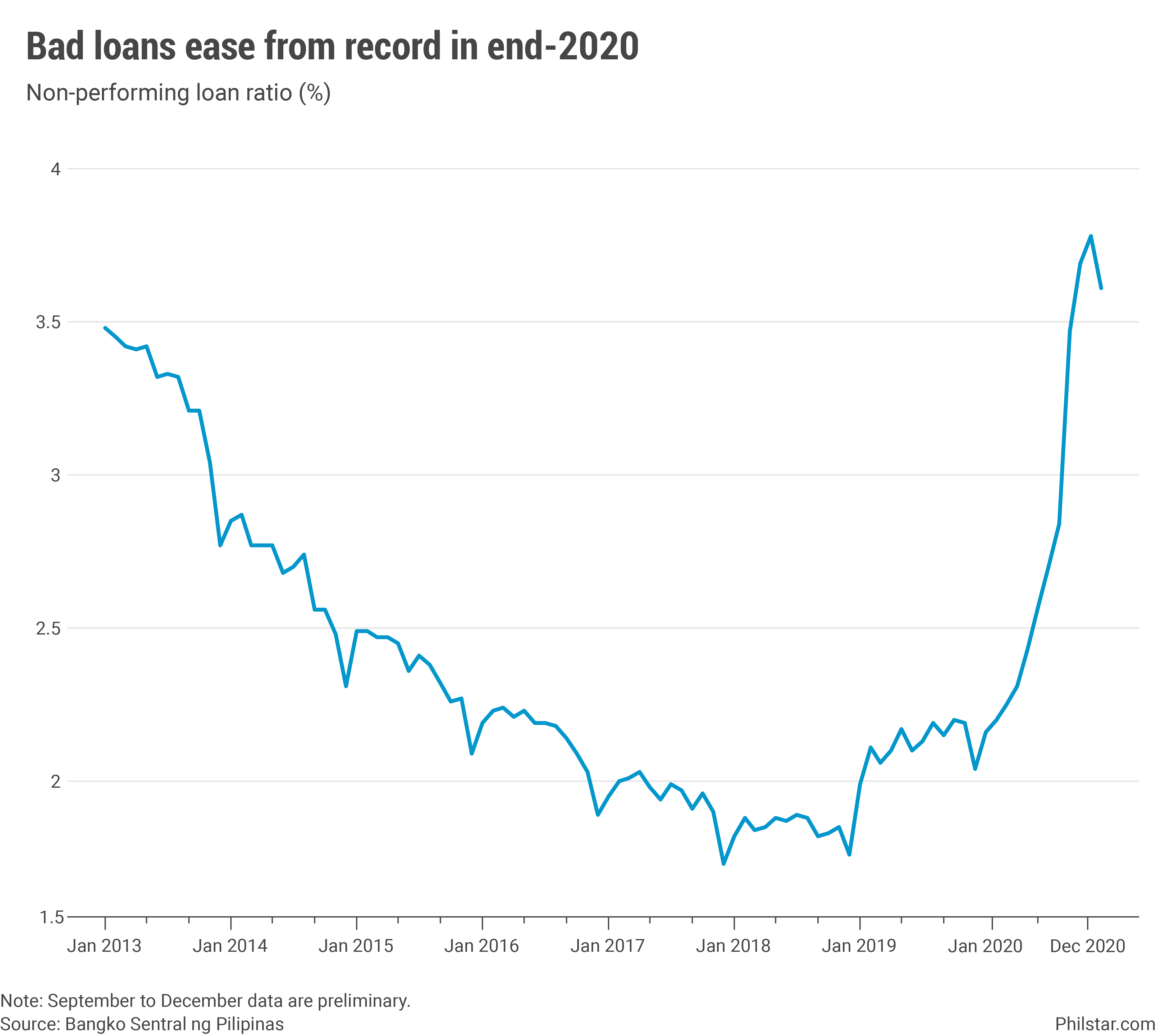

Gross non-performing loans, or those which remained unpaid for at least 30 days past due date, inched down 2.3% from previous month to P391.66 billion in end-December, central bank data showed on Monday.

As a proportion of the entire loan book, local banks’ bad debt ratio eased from record-high to close 2020 at 3.61%, although up from 2.04% a year ago. The preliminary figure was also below the 4.6% NPL ratio expected by lenders themselves in a survey by the Bangko Sentral ng Pilipinas (BSP).

The surprise last-minute slide in NPL coincided with the expiration of moratorium in loan payments provided for under Bayanihan to Recover As One Act last year, and therefore likely represented one-off payments to outstanding balances to avoid paying penalties.

Emilio Neri Jr., lead economist at Bank of the Philippine Islands, expects NPL to resume its uptrend in the first quarter. “NPLs will likely rise in 1Q and banks will likely provision even more…,” Neri said in an email before the data was released.

Indeed, following months of decline to cover losses from rising bad debts, lenders have restarted setting aside more funds to protect their balance sheets. The so-called NPL coverage ratio rose to 93.73% in December, the highest since August.

An elevated amount of unpaid loans would continue to prevent banks from lending to consumers and businesses as warranted by government to propel recovery. BSP had eased benchmark rates used to price loans by an aggressive 200 basis points last year, yet lending had been dismal and even fell for the first time in 14 years in December.

“I’m still seeing banks to be cautious but more optimistic versus 2020…But no doubt they are still cautious than normal,” Patrick Ella, economist at Sun Life of Canada (Philippines) Inc., said in a separate email.

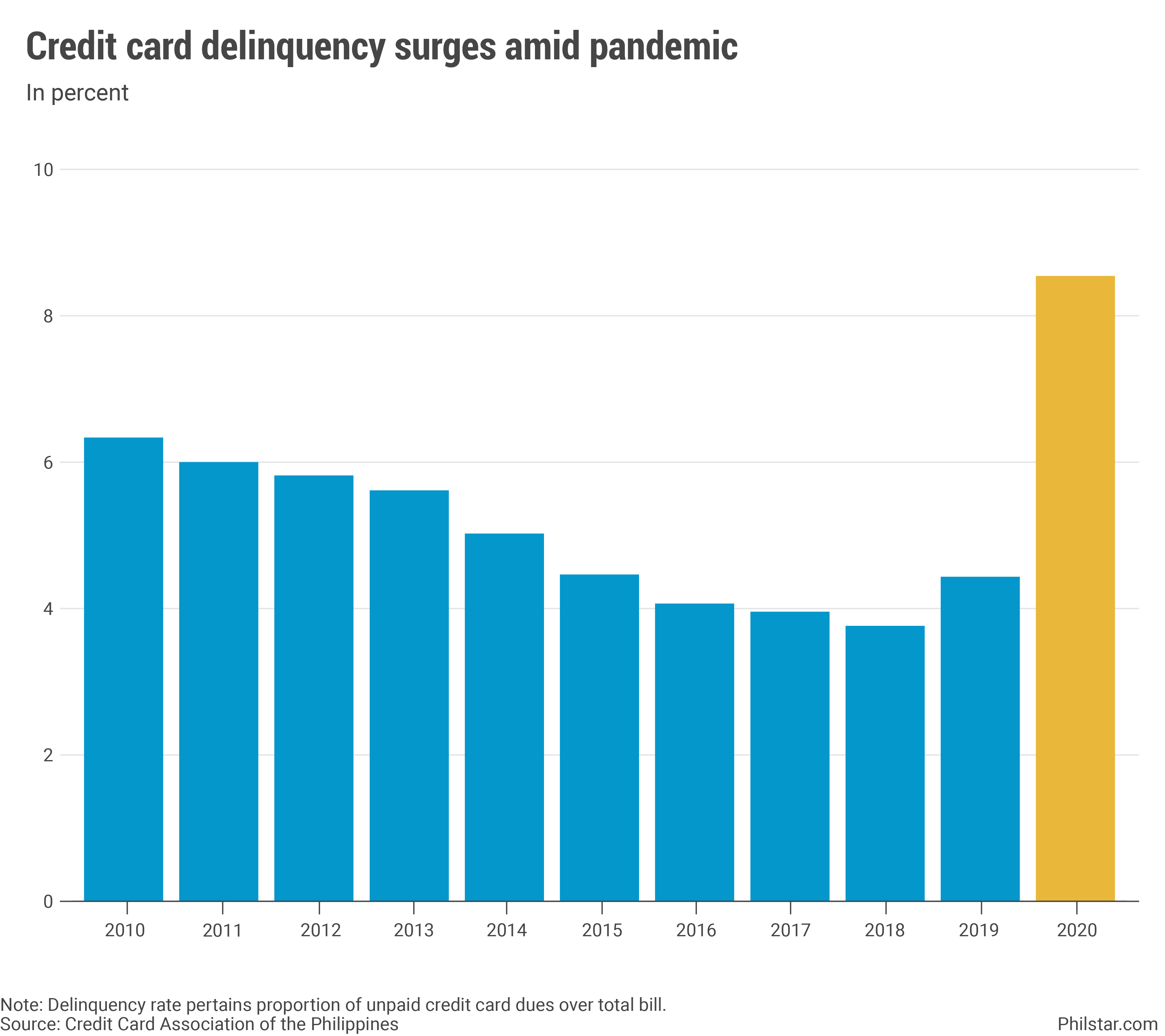

Improvements in headline NPL, however, masked worsening credit profiles across different loan types. For instance, credit card defaults proliferated last year, pushing up the delinquency rate to 8.4% in December, separate data from the Credit Card Association of the Philippines showed.

That marked the highest since at least 2010, the latest available record provided. At the time, two years after the global financial crisis, the delinquency rate stood at 6.23%.

The delinquency rate is the proportion of unpaid credit card dues over the total outstanding bill. Credit card delinquency occurs when a cardholder has poor payment history and frequently pays bills way past due date. The credit limit of delinquent borrowers are also often maxed out, which may be a sign of strained income.

Banks' distressed assets, which includes foreclosed properties as well as restructured loans, also continued to increase by 8.7% month-on-month to P680.19 billion. As a proportion of loans and properties, distressed assets ratio hit 6.19%, nearly double from end-2019's 3.23%.

The government is banking on the Financial Institutions Strategic Transfer (FIST) bill to remove the burden from soured debts on banks so that they can lend out. Under the measure, FIST institutions may be established, whose task will be to buy out unpaid credit, seeking payment from borrowers, or if not, ultimately dispose them off.

But Neri said FIST, which is awaiting signature from the president, is unlikely to encourage lenders to take in more risk by lending more. “The amount allocated for FIST is less than 1% of GDP (gross domestic product) and unlikely to have a meaningful effect on how industry lends to SMEs,” he said.

- Latest

- Trending